Todd Maiden

Wednesday, November 6, 2024

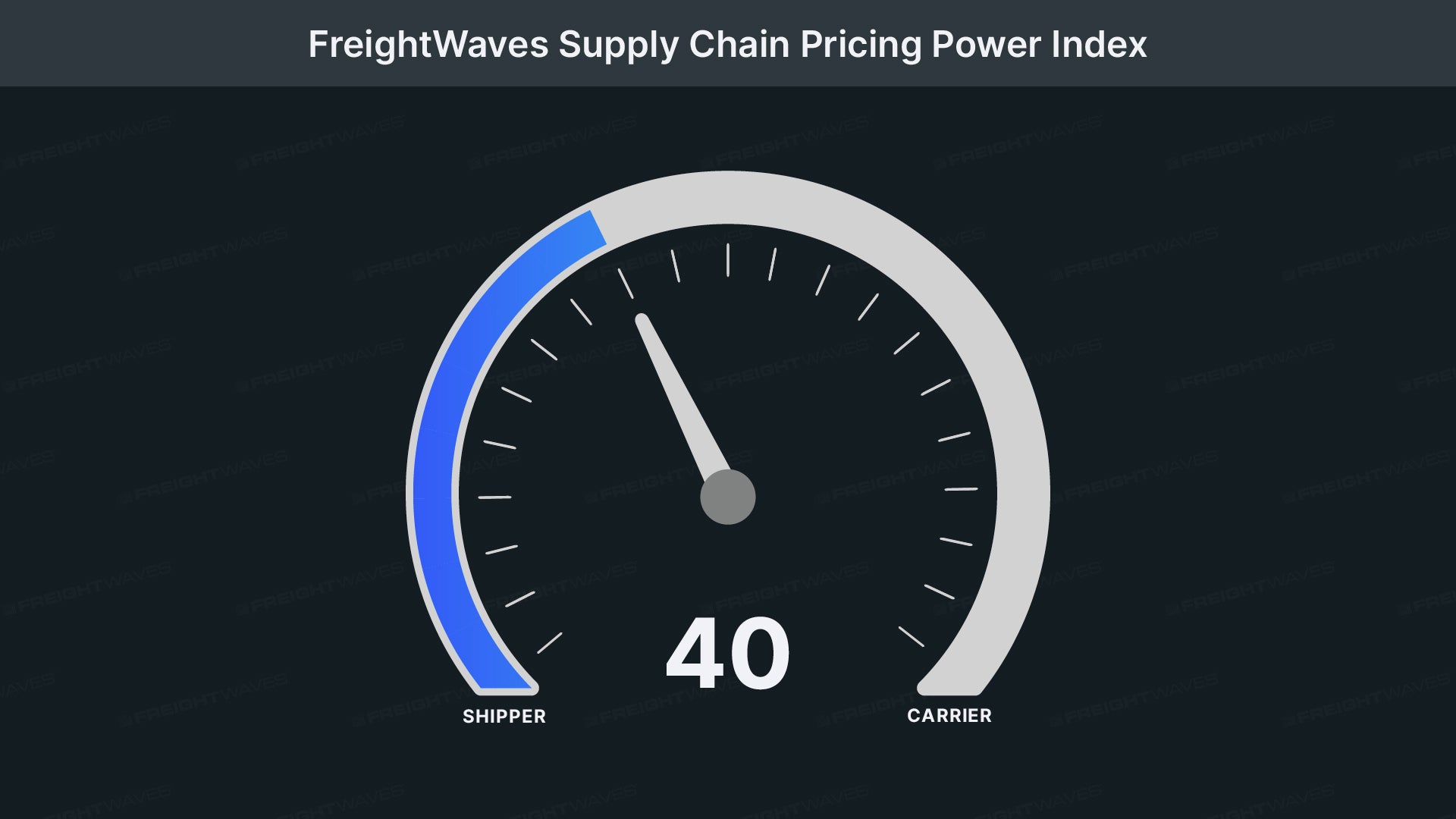

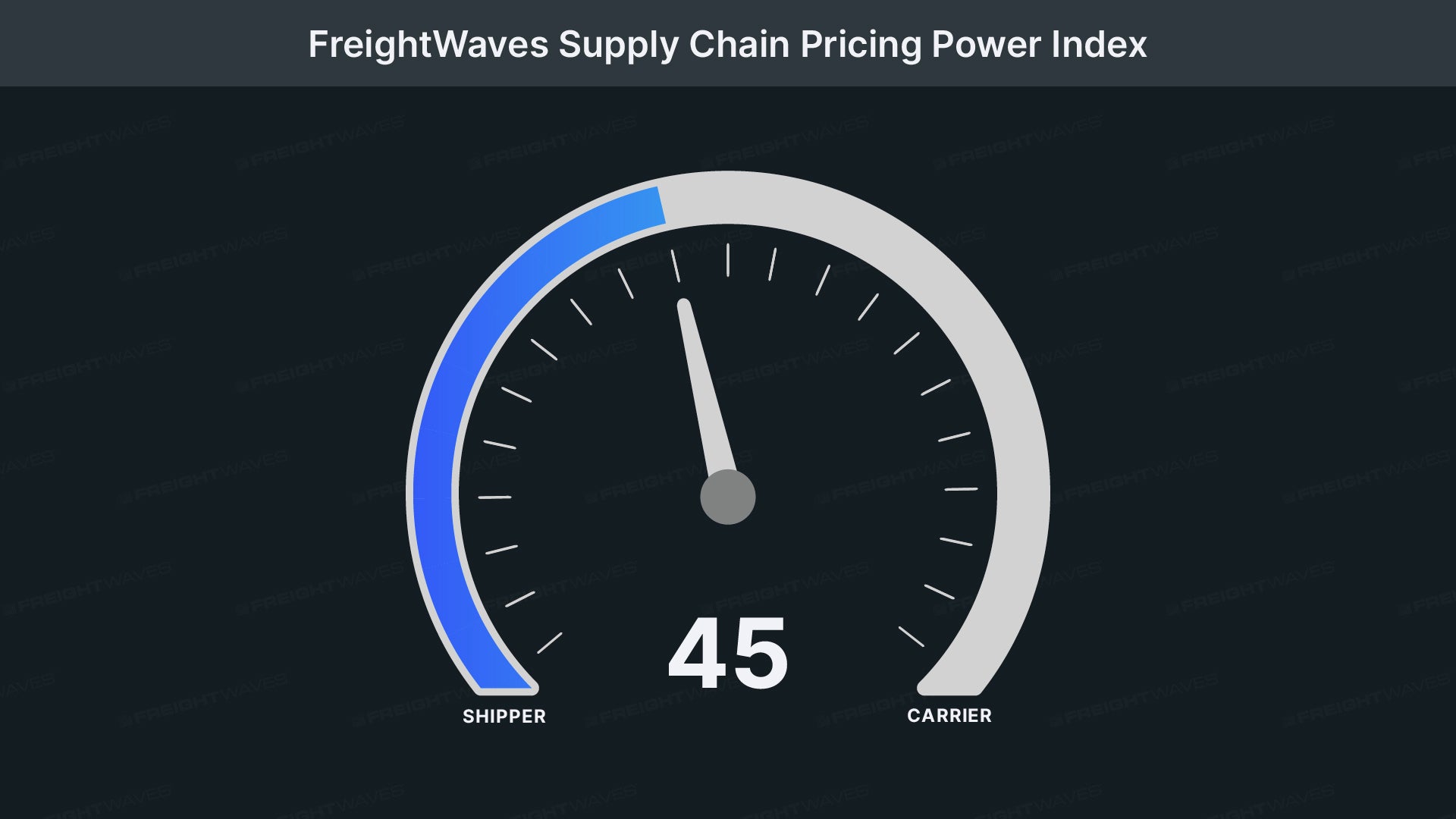

Schneider National cuts outlook, ‘commoditized’ one-way fleet uninvestable

Schneider National is hopeful for a better seasonal inflection in the fourth quarter, noting some areas of the truckload market are seeing significant capacity exits.