Other FreightWaves Products

Nov

- 2024 -

08 November

Michael Rudolph

Read More »

Freight markets brace for impact of proposed tariffs

For months now, it has been clear that shippers have frontloaded record imports to the country, largely to avoid expected tariffs.

Oct

- 2024 -

01 October

Michael Rudolph

Read More »

SONAR White Paper: What freight data tells us about an ILA port strike

From ocean container flows to intermodal rail movements and truckload tenders, our white paper lays out the impact of the port strike.

Sep

- 2024 -

23 September

Michael Rudolph

Read More »

FreightWaves announces 2025 FreightTech 100 companies

FreightWaves has unveiled its 2025 FreightTech 100 list, spotlighting tech-forward companies that have best navigated a turbulent year.

11 September

Michael Rudolph

Read More »

ILA readiness to strike highest since 2012

Solidarity between the ILA and ILWU was on display the last time the ILA narrowly avoided a strike (and the ILWU did not).

10 September

Michael Rudolph

Read More »

Half a century later, ILA returns to strike mode

The ILA maintains that it will not accept any extension of their current contract nor any potential mediation by the federal government.

Jun

- 2024 -

05 June

Michael Rudolph

Read More »

ANALYSIS: ATA’s Chris Spear earns $1.9M, but where are his results?

Based on its results this Congress, the American Trucking Associations’ lobbying efforts make it look less like a Machiavellian operator and more like another Washington grifter.

Apr

- 2024 -

15 April

Michael Rudolph

Read More »

Panama Canal’s future is dark and stormy, much to shippers’ relief

The end of Panama’s dry season is in sight, and the Panama Canal Authority plans to welcome more vessels in the coming weeks.

08 April

Michael Rudolph

Read More »

Demand shocks keeping aging fleets afloat, argue shipowners

Ship recycling has fallen to its lowest level in 20 years, per a recent report by the Baltic and International Maritime Council.

01 April

Michael Rudolph

Read More »

Red Sea crisis nears boiling point, unable to heat up spot rates

If China and Russia find the Houthi problem in the Red Sea as intractable as the U.S. and its allies have, it would all but halt what little maritime traffic remains in the region.

Mar

- 2024 -

29 March

Michael Rudolph

Read More »

Mississippi River shipping faces potential crisis for third straight year

An unusually warm and dry winter might herald drought conditions in key areas of the Mississippi River Basin over the coming months.

01 March

Michael Rudolph

Read More »

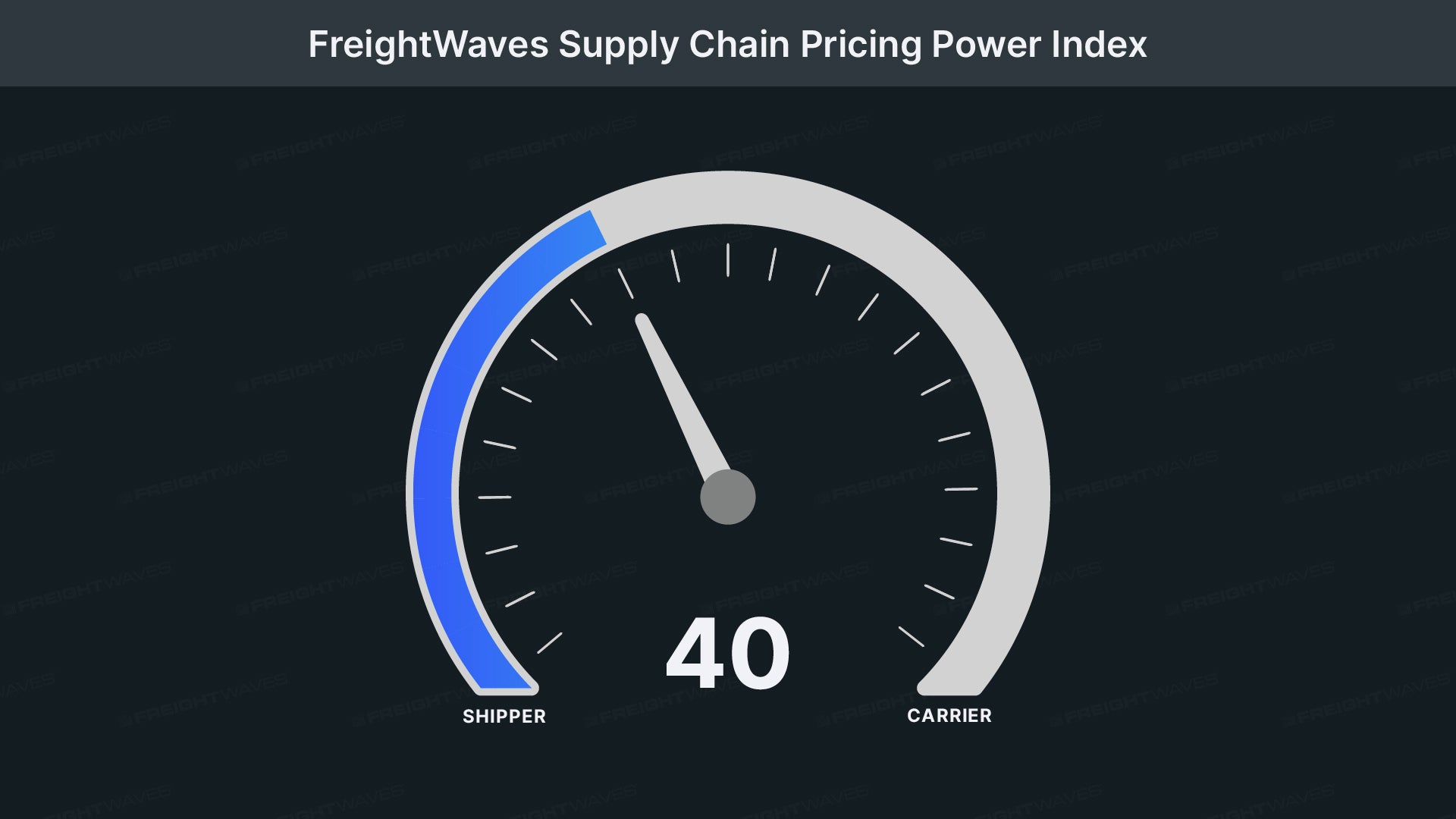

Beware the false spring

Even as carriers’ pricing power deteriorated, freight demand was consistently robust throughout February.

Feb

- 2024 -

26 February

Michael Rudolph

Read More »

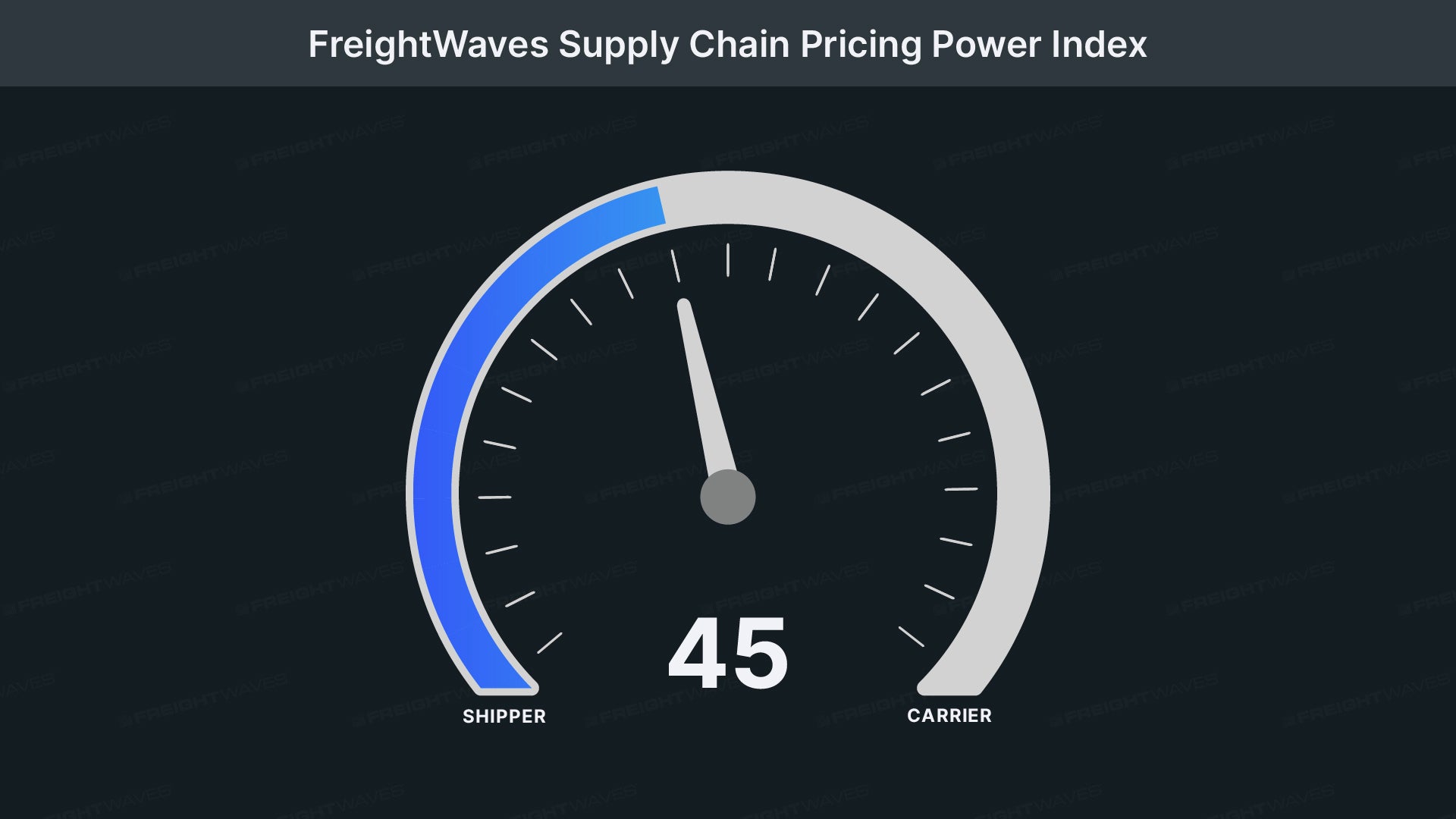

Threat of strike looms large over East, Gulf Coast ports

Dockworkers are fully prepared to swap pallet jacks for picket signs come October.

19 February

Michael Rudolph

Read More »

War risk exclusions by insurers heighten stakes in Red Sea attacks

A recent string of Houthi attacks have reignited concerns about the Red Sea crisis, raising the floor for tanker rates.

12 February

Michael Rudolph

Read More »

Despite dim outlook, January imports grew at fastest pace in 7 years

A rise in Chinese imports indicates seasonal trends are playing out as usual, very much unlike 2023’s anemic performance.

09 February

Michael Rudolph

Read More »

The long road to recovery

The early stages of this recovery are characterized by a rebalancing market, a return to normalcy after a four-year roller coaster of volatility.

05 February

Michael Rudolph

Read More »

Red Sea turmoil drives Chinese exporters to rail, other alternatives

A recent round of U.S. and British strikes raise fresh questions about the impact of container shipping in the Red Sea.

Jan

- 2024 -

12 January

Michael Rudolph

Read More »

Crosswinds threaten soft landing

The sustained imbalance between supply and demand has yet to be corrected, such that only an unprecedented tidal wave of demand could satisfy the current amount of capacity in the national freight economy.

05 January

Michael Rudolph

Read More »

Better late than never

Spot rates did eventually see a boost at the start of the new year, albeit one that was unable to meet our prior forecasts.

Dec

- 2023 -

15 December

Michael Rudolph

Read More »

It’s beginning to look a lot like … 2021?

Tender volumes began to outpace 2020 earlier this week and are now marching toward favorable comparisons with 2021.

08 December

Michael Rudolph

Read More »

Steady as she goes

Volumes are leveling out at the start of December, delaying the seasonal dip that ordinarily occurs at this time of the year.

01 December

Michael Rudolph

Read More »

The most wonderful time

Tender volumes were outpacing 2022 levels before the holiday and came within spitting distance of 2020 — freight demand’s second-best year on record.

Nov

- 2023 -

10 November

Michael Rudolph

Read More »

The minor fall and the major lift

This week, freight markets underwent a surprising rally that saw a wave of volumes sweep across the country.

03 November

Michael Rudolph

Read More »

Death by a thousand cuts

Domestic manufacturers fail to inspire optimism, since they foresee major headwinds on output in the first half of 2024.

Oct

- 2023 -

27 October

Michael Rudolph

Read More »

Pumping the brakes

The upcoming months are littered with major holidays during which carriers can leverage seasonal constraints on capacity for higher spot rates.

20 October

Michael Rudolph

Read More »

Seasonal depression

Outside of the holiday rush periods, the fundamental lack of freight demand will continue to expose the lingering overcapacity in the market.

13 October

Michael Rudolph

Read More »

Business as usual?

Given the surplus of available capacity, shippers are more confident in switching to “just-in-time” freight strategies as consumer resilience remains an open question.

Sep

- 2023 -

29 September

Michael Rudolph

Read More »

Under pressure

By next week, it is likely that actual freight flow will have finally risen on a yearly basis for the first time since May 2022.

22 September

Michael Rudolph

Read More »

Playing the waiting game

Consumer demand during the holiday season is expected to be relatively soft, which should temper expectations for a red-hot peak season in truckload markets.

15 September

Michael Rudolph

Read More »

Reading the tea leaves

Perhaps the most pressing question for both freight markets and the broader economy is how the consumer will fare in the coming months.

08 September

Michael Rudolph

Read More »

Markets clock out on Labor Day

Rejection rates gathered some promising momentum in the run-up to Labor Day, though these gains are slowly being lost.

01 September

Michael Rudolph

Read More »

Back despite popular demand

After a none-too-brief break, the Pricing Power Index is resuming its regular Friday schedule.

Jul

- 2023 -

28 July

Michael Rudolph

Read More »

Unfasten your seat belts

Against significant odds, the Federal Reserve might realize its once-unlikely goal of a “soft landing” — that is, taming inflation without also triggering a recession.

14 July

Michael Rudolph

Read More »

Bottom’s up!

Demand from retail shippers is historically quiet in the period from now until August, after which retailers restock their shelves for the back-to-school season.

07 July

Michael Rudolph

Read More »

Summer’s lease has all too short a date

Demand from retail shippers is historically quiet in the period from now until August, after which retailers restock their shelves for the back-to-school season.

Jun

- 2023 -

30 June

Michael Rudolph

Read More »

No freight market fireworks in 2023

Maritime’s peak season — which typically ramps up in August and lasts throughout October — is expected by retailers and supply chain professionals to be weaker than it has been in previous years.

09 June

Michael Rudolph

Read More »

No cure for the summertime blues

Tender rejections have yet to return to mid-May’s all-time low, but their softness could persist in a trough for the next two quarters.

02 June

Michael Rudolph

Read More »

June bugs and gold bugs

One last round of bad news to cap this week: China and the U.S. both posted dismal data from their respective industrial economies.

May

- 2023 -

26 May

Michael Rudolph

Read More »

Memorial Day might instead signal mayday

Volumes did see some growth ahead of the upcoming Memorial Day holiday, though not nearly enough to bust out the champagne and sparklers.

19 May

Michael Rudolph

Read More »

Puttin’ on the Blitz

So as not to bury the lede, this week’s lack of change in the PPI might ultimately prove to be the most exciting stability in quite some time.

12 May

Michael Rudolph

Read More »

May flowers wither on the vine

Despite expectations for seasonal growth in the second quarter, the health of the American consumer has continued to become more precarious, stirring headwinds for even once-reliable sources of freight.

Apr

- 2023 -

28 April

Michael Rudolph

Read More »

The more things change …

Volumes are just beginning to tick up at the tail end of April, but freight demand in the quarter has been mostly flat and thus grossly unseasonable.

07 April

Michael Rudolph

Read More »

No motion in the ocean (markets)

While ocean carriers are not facing the same risks as their domestic trucking counterparts, given their consolidation and enormous war chests, ocean’s weakness in demand will continue to trickle down into truckload markets.

Mar

- 2023 -

31 March

Michael Rudolph

Read More »

Too early for an April Fools’ joke

Despite seeing slight seasonal growth, truckload markets are showing a continued soft patch.

24 March

Michael Rudolph

Read More »

Empty wallets threaten seasonal growth

The gap between current levels of freight demand and those of 2019 is narrowing, casting doubt on the market’s ability to sustain growth.

17 March

Michael Rudolph

Read More »

Freight markets are stuck in the doldrums

The consumer will be key to resolving the present tension in freight demand’s future, but consumers continue to be predictably unpredictable.

10 March

Michael Rudolph

Read More »

The calm before the storm

Market conditions will likely become a bit more favorable before they get much worse.

03 March

Michael Rudolph

Read More »

La estacionalidad no puede salvar un mercado maltrecho

Índice de poder de fijación de precios de la cadena de suministro FreightWaves de la semana pasada: 30 (Cargadores) Perspectivas a tres meses del Índice FreightWaves de Poder de Compra […]

Michael Rudolph

Read More »

Seasonality can’t save a battered market

Strangely enough, tender volumes are abiding by seasonal trends.

Feb

- 2023 -

17 February

Michael Rudolph

Read More »

Bears and bulls duke it out, signaling hazard

Strangely enough, tender volumes are abiding by seasonal trends. The first quarter of 2022 was unusually active as shippers tried to get ahead of disruptions to capacity, which historically tightens in the spring.

10 February

Michael Rudolph

Read More »

Risky business throttles cruise control

With the inflation-squeezed consumer running through their discretionary budgets, freight demand is in a precarious state.

03 February

Michael Rudolph

Read More »

Spot markets are flatlining

Consumers’ appetite for discretionary spending has been usurped in favor of squirreling away income into personal savings.

Jan

- 2023 -

27 January

Michael Rudolph

Read More »

Markets are bad, but they could be worse

Volumes have continued their recovery from the winter holiday season with a surge in pent-up freight demand unleashed into the market. Naturally, since last week’s data was affected by holiday noise, the Outbound Tender Volume Index (OTVI) faces some absurdly easy comps on a weekly basis. Even still, accepted tender volumes remain below their levels of 2021 and ’22 for the time being.

13 January

Michael Rudolph

Read More »

Freight outlook for January is grim but seasonal

Volumes have continued their recovery from the winter holiday season with a surge in pent-up freight demand unleashed into the market. Naturally, since last week’s data was affected by holiday noise, the Outbound Tender Volume Index (OTVI) faces some absurdly easy comps on a weekly basis. Even still, accepted tender volumes remain below their levels of 2021 and ’22 for the time being.

06 January

Michael Rudolph

Read More »

Freight markets stir after holiday slumber

For all intents and purposes, the month of December has only three weeks of freight activity, as the final week from Christmas to New Year’s is effectively null. In years prior, freight demand has fallen throughout the month before bottoming out in that final week. So far, December looks to be following seasonal trends, which is to say that, while shippers’ activity is winding down, this movement is not alarming by itself. Rather, the gap in freight demand between 2022 and ’21 (or even ’20) is the main symptom of current ailments.

Dec

- 2022 -

16 December

Michael Rudolph

Read More »

Current trends give a sneak peek into weak 2023

For all intents and purposes, the month of December has only three weeks of freight activity, as the final week from Christmas to New Year’s is effectively null. In years prior, freight demand has fallen throughout the month before bottoming out in that final week. So far, December looks to be following seasonal trends, which is to say that, while shippers’ activity is winding down, this movement is not alarming by itself. Rather, the gap in freight demand between 2022 and ’21 (or even ’20) is the main symptom of current ailments.

09 December

Michael Rudolph

Read More »

Contract market contracts, squeezing larger carriers

Contrary to popular opinion, December is not a peak season for freight. True, the freight that needs to be moved in this month typically has greater urgency than usual, which does put upward pressure on carrier rates. But peak truckload volumes are largely influenced by maritime imports, which historically peak between July and September.

02 December

Michael Rudolph

Read More »

Freight markets are feeling an early freeze

Historically, November is the month in which maritime imports begin to move inland for their final push before the holiday shopping season. Yet such imports were lost at sea this year, failing to materialize during ocean shippers’ peak season. This one-two punch of weakened import volumes and overstocked retail inventories means that carriers are left with fewer opportunities to source freight.

Nov

- 2022 -

18 November

Michael Rudolph

Read More »

Holiday gains are nowhere in sight

Historically, November is the month in which maritime imports begin to move inland for their final push before the holiday shopping season. Yet such imports were lost at sea this year, failing to materialize during ocean shippers’ peak season. This one-two punch of weakened import volumes and overstocked retail inventories means that carriers are left with fewer opportunities to source freight.

11 November

Michael Rudolph

Read More »

Middling markets show no signs of peaking

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

Oct

- 2022 -

28 October

Michael Rudolph

Read More »

Carriers get their freight frights just in time

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

14 October

Michael Rudolph

Read More »

Carriers’ pricing leverage suffers a harsh blow

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

Sep

- 2022 -

30 September

Michael Rudolph

Read More »

Freight markets see little change this week

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

23 September

Michael Rudolph

Read More »

Truckload markets resume their decline

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

16 September

Michael Rudolph

Read More »

The market shakes off its holiday hangover

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

09 September

Michael Rudolph

Read More »

Freight clocks out for Labor Day

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

02 September

Michael Rudolph

Read More »

Freight demand, rejection rates remain relatively stagnant

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

Aug

- 2022 -

19 August

Michael Rudolph

Read More »

Chicken Little is proved to be an optimist

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

12 August

Michael Rudolph

Read More »

Industry eyes are wide shut

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

05 August

Michael Rudolph

Read More »

Contract rates are puzzling; tender rejections flirt with sub-6% levels

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

Jul

- 2022 -

22 July

Michael Rudolph

Read More »

Have contract rates begun their Q3 decline?

Since the pandemic started, many shippers found their existing contracts unable to ensure carrier compliance. Supply and demand were especially volatile, and so spot rates, which are more sensitive to changing market conditions, handily outpaced contract rates.

15 July

Michael Rudolph

Read More »

Small carriers are facing pressure from multiple sources

In the nine days since July began, OTRI fell 141 basis points (bps) to its lowest level in over two years: 6.7%. In the three days following that bottom, OTRI clawed back 50 bps. At present, however, it seems as though any upward momentum upon which it could have built has been lost.

14 July

Michael Rudolph

Read More »

When (and by how much) will shippers shift to the spot market?

After a record year of freight demand in 2021, carriers playing in the spot market benefited from a blank check when naming rates. The federal stimulus enabled consumers to pay […]

08 July

Michael Rudolph

Read More »

Freight demand takes summer dip as rejection rates tumble

Volume levels are depressed this week by Monday’s holiday. The national average rate of tender rejections sunk below 7% late in the week, but linehaul spot rates…

01 July

Michael Rudolph

Read More »

In the last week of Q2, freight demand rises only slightly

Volume levels have made a final push before the second quarter ends. The national rejection rate has recovered from its earlier dip below 8%…

Jun

- 2022 -

24 June

Michael Rudolph

Read More »

Rejection rates continue to fall, leading to depression in the spot market

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 8%…

17 June

Michael Rudolph

Read More »

Freight demand succumbs to headwinds as spot rates continue to slide

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 9%…

10 June

Michael Rudolph

Read More »

Volumes recover from post-holiday depression, rejections take a dive

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 9%…

08 June

Michael Rudolph

Read More »

Agentes de carga: ¿Cómo se mide su salario?

En la era del trabajo a distancia, aprovechar las ubicaciones comerciales de menor costo puede liberar dinero para una mayor compensación

Michael Rudolph

Read More »

Freight brokers: How does your pay measure up?

A FreightWaves survey of freight brokers found significant differences in entry-level base pay and commission rates by region.

03 June

Michael Rudolph

Read More »

Memorial Day throws off tender volumes and rejection rates this week

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 9%…

May

- 2022 -

27 May

Michael Rudolph

Read More »

Volume levels and rejection rates rally in time for Memorial Day weekend

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 9%…

20 May

Michael Rudolph

Read More »

Volumes, rejections and rates crab walk the market to a low boil

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 9%…

13 May

Michael Rudolph

Read More »

Volumes are flatlining as spot rates slide further

Volume levels have restarted their decline, as have spot rates. The national rejection rate has fallen below 9%…

06 May

Michael Rudolph

Read More »

Falling tender volumes erase most of last week’s gains

Volume levels have restarted the decline after recovering after Easter Weekend. The national rejection rate has fallen below 9%…

Apr

- 2022 -

29 April

Michael Rudolph

Read More »

Shippers are back in the driver’s seat on rates

Tender volumes and tender rejection rates are both on a rapid decline, signaling trouble for the truckload market. Carriers and shippers alike will need to…

08 April

Michael Rudolph

Read More »

Accepted tender volume rebounds over year-ago levels against soft comps

Tender volumes and tender rejection rates are both on a rapid decline, signaling trouble for the truckload market. Carriers and shippers alike will need to…

01 April

Michael Rudolph

Read More »

National tender rejections nose-dive as freight demand decline continues

Tender volumes and tender rejection rates are both on a rapid decline, signaling trouble for the truckload market. Carriers and shippers alike will need to…

Mar

- 2022 -

25 March

Michael Rudolph

Read More »

National tender rejection rates fall under 16% for first time in nearly 2 years

Both tender volumes and tender rejection rates take a breather over the past week. It’s too early to be called a trend but definitely…

18 March

Michael Rudolph

Read More »

Freight volume is deflated by rising costs against seasonal expectations

Both tender volumes and tender rejection rates take a breather over the past week. It’s too early to be called a trend but definitely…