Michael Rudolph

Friday, November 8, 2024

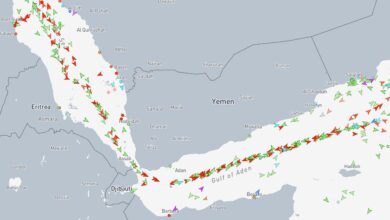

Freight markets brace for impact of proposed tariffs

For months now, it has been clear that shippers have frontloaded record imports to the country, largely to avoid expected tariffs.